Without the burden of student loans, you can fully invest time and energy into your career.

Takeaways:

- Calculating your debt-to-income ratio is the first step to properly understanding your student loan situation.

- Enrolling in an income-driven repayment plan while pursuing loan forgiveness and grants is a good option if you have a high debt-to-income ratio.

The journey to eliminating your nursing school debt can be a long one, but that doesn’t mean it has to be difficult. In fact, the sooner you’re on the right path, the sooner you’ll enjoy lower stress levels. Determining the best option to eliminate your loans depends almost entirely on two things: the amount of debt you owe and the amount of income you earn. Without putting your debt amount into the context of your income, you won’t be able to identify the best way forward. To do this, you’ll need to calculate your debt-to-income ratio.

Debt-to-income ratio calculation

This calculation is simple and quick to perform: Add up all the school loans you have, then divide that number by your income (pre-tax). If you’re still in school, estimate how much debt you’ll have when your degree is complete and your future salary. For example, if you have $84,000 in school loans and your income is $70,000, the calculation would be: Debt/Income = $84,000/$70,000 = 1.2. (See Debt-to-income ratio recommendations.)

If you’re part of a two-income household with joined finances and you share each other’s debts and incomes, perform this calculation together and use that new ratio to guide your debt payoff plan.

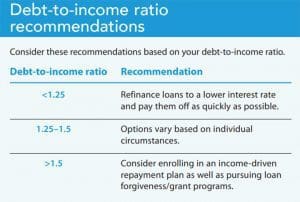

Debt-to-income ratio <1.25

If your debt-to-income ratio is <1.25, your goal should be to pay off your loans as quickly as possible to save time and money paid on the interest. Start by refinancing your loans to a lower interest rate, which has the added benefit of consolidating all of the refinanced loans into one place. This simplification has psychological benefits because now you have only one or two loans to pay extra toward.

Most student loans have 10-year payment terms, but you should refinance your loans to a term length equal to time remaining or less. For instance, if you have 8 years left on your loans and they haven’t been refinanced, refinance them to 8 years or less. Longer terms will result in paying more money over time and delay your debt elimination. The next step is to pay extra toward your principal loan balance, which is the amount due on your student loan debt before interest. Making extra principal payments is the most efficient way to pay down your loans faster and pay less in interest.

To pay extra, you’ll need to either reduce your spending in other areas or increase your income with overtime or per diem work. The key to successfully working extra is avoiding burnout, and the key to reducing your spending is keeping your fixed costs low. Fixed costs are consistent recurring expenses such as rent or mortgage payments, car payments, and utility bills. The higher these are, the less financial flexibility you have to pay off your student loans and save for retirement or a significant life event. For example, I recommend keeping your monthly housing payment at less than 30% of your take-home pay; car payments should be less than 10%. This gives you enough room in the rest of your budget to make extra loan payments. Remember, every dollar of spending you eliminate from other areas of your budget frees up a dollar to go toward your loans. Also consider temporarily reducing spending in other areas, such as eating out, shopping, or vacations.

However you choose to pay more toward your loans every month, it’s best to automate the process as much as possible. If you can’t set up automatic additional monthly payments, then set up a recurring automatic transfer from your checking account to a separate account where you make extra payments. This way, you’ll be less tempted to spend the money slotted for your debt payoff plan.

To see the impact of paying extra every month, use my debt payoff calculator. The calculator can help you with goal setting and staying on track.

Debt-to-income ratio of 1.25–1.5

The best route for eliminating your school loans with a ratio in this range varies among individuals. If you have no other debt, are highly motivated to eliminate your loans, are frugal, or plan to work overtime to pay them off quicker, follow the <1.25 recommendations described above. If you have substantial other debt, don’t mind working for a nonprofit hospital for the next 10 years, aren’t frugal, or don’t plan to work overtime, follow the >1.5 recommendations below.

Debt-to-income ratio >1.5

A high debt-to-income ratio may appear to be the most challenging, but surprisingly it’s the most straightforward to address because the higher your ratio, the fewer options you have for eliminating the debt.

When your ratio goes above 1.5, your monthly loan payment is large enough that it will be exceedingly difficult to pay extra toward your loans and live a reasonably comfortable lifestyle. For example, if you make $70,000 and you owe $115,000, your debt-to-income ratio is 1.64 and your monthly loan payment would be approximately 30% of your take-home pay every month. That’s like having an extra rent or mortgage payment. In addition, after you factor in all the other living costs and recurring monthly expenses, you’ll likely have very little flexibility in your budget.

If your ratio is >1.5, I recommend you seriously consider enrolling in an income-driven repayment (IDR) plan and pursue loan forgiveness and grants.

IDR plan: For federal student loans that haven’t been refinanced, you can enroll in an IDR plan that will reduce your monthly payment significantly, sometimes as much as 50%. The government reduces your monthly payment to a percentage of your discretionary income based on your family size, geographic location, and income level.

This reduced monthly payment is ideal for those pursuing loan forgiveness and grants, which base the amount they forgive or pay off on a percentage of the remaining loans. Paying as little as possible until you receive forgiveness is the name of this game. The potential downside is that if you enroll in an IDR Plan and don’t pursue loan forgiveness, you’ll be in debt significantly longer. IDR loan lengths typically are 20 to 25 years instead of the customary 10, which means you wouldn’t save much money over the life of your loans. To learn more about IDRs, visit studentaid.gov/manage-loans/repayment/plans.

Public Service Loan Forgiveness (PSLF): This program forgives federal un-refinanced loans after you complete 10 years of qualifying payments while working for a nonprofit (501c3) hospital. Private loans, as well as federal loans that you’ve already refinanced, don’t qualify for forgiveness. To pursue PSLF, you must enroll in an IDR plan.

Nurse Corps Loan Repayment Program (NCLRP) + National Health Services Corps (NHSC) Loan Repayment Program: These Health Resources & Services Administration (HRSA) programs require that you work for a defined length of time at a qualifying facility or location. Eligible workplaces include those in underserved communities, those with critical shortages, and even some schools of nursing.

The NCLRP will forgive up to 85% of your loans (60% after 2 years of service and possibly 25% more for a third year). This program is based on need, so not everyone is eligible. However, it’s worth applying for it while pursuing PSLF. The NHSC will pay $25,000 to $50,000 of your loans after an initial 2-year term. Learn more about these and other HRSA programs at nhsc.hrsa.gov.

Many states and employers also offer loan payoff or bonuses to help recruit and retain qualified nurses. Military service and Perkins Loan cancellation are worthy of consideration as well.

Bottom line

For many of us, school loans are unavoidable on our path to becoming nurses or furthering our careers. Creating a clear plan to eliminate those loans will allow you to enjoy exactly why you got into nursing to begin with—a satisfying career where you routinely use your knowledge, skills, and experience to improve the lives of others.

Matt Soladay, creator of Scrubs Money Life blog, is a pediatric nurse anesthetist in Baltimore, Maryland.

Resources

Tap into these resources to learn more about repaying student loans and paying more toward your debt.

Federal Student Aid

- Understand student loan repayment: Learn about repayment based on where you are in the process. studentaid.gov/h/manage-loans

- Choose the federal student loan repayment plan that’s best for you: Learn about different types of repayment plans. studentaid.gov/manage-loans/repayment/plans

- Load simulator: Enter your loan information to find out which repayment plan may be best for you. studentaid.gov/loan-simulator

- Public Service Loan Forgiveness: Those employed by a U.S. federal, state, local, or tribal government or a nonprofit organization may be eligible for this program. studentaid.gov/manage-loans/forgiveness-cancellation/public-service

- Income-Driven Repayment plan request: If you need to make lower monthly payments or your outstanding federal student loan debt represents a significant portion of your annual income, you may be eligible for an income-driven plan. studentaid.gov/app/ibrInstructions.action

Health Resources & Services Administration (HRSA)

- Apply for loan repayment: Learn about HRSA loan program offerings. bhw.hrsa.gov/funding/apply-loan-repayment

- Apply to the Nurse Corps Loan Repayment program: Learn about and apply for this repayment program. bhw.hrsa.gov/funding/apply-loan-repayment/nurse-corps

- NHSC Loan Repayment program: Learn about and apply for the National Health Service Corps program. nhsc.hrsa.gov/loan-repayment/nhsc-loan-repayment-program

ScrubsMoneyLife

- Debt payoff calculator: Use this tool to determine the impact of paying extra toward your student loan debt. scrubsmoneylife.com/debt-payoff-calculator